LAB 8: MARKET WEEKLY REPORTS AND CUBIC SPLINE INTERPOLATION

Mathematics:

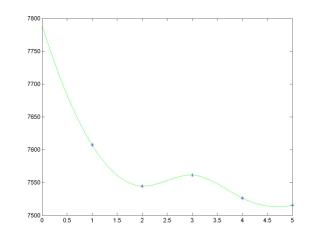

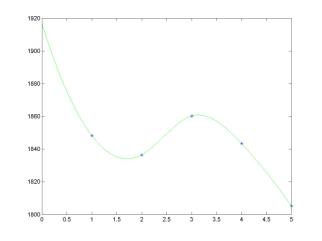

Interpolation problems are problems of finding a curve that passes through specified points in the plane. Fitting a curve through points in the plane encounters commonly in analyzing experimental data, in ascertaining the relations among variables and in design work. This project exploits ideas of piecewise cubic spline interpolation for a presentation of market weekly data in the form of a smooth "well-behaved" curve. For the week of February 11-15, 2002, the market indices were registered at the closing bells as follow:

Toronto Stock

Exchange 300:

|

Day of Week |

Monday |

Tuesday |

Wednesday |

Thursday |

Friday |

|

Index Value |

7607.40 |

7544.60 |

7561.20 |

7526.40 |

7515.30 |

Nasdaq Index:

|

Day of Week |

Monday |

Tuesday |

Wednesday |

Thursday |

Friday |

|

Index Value |

1848.20 |

1836.50 |

1860.20 |

1843.40 |

1805.20 |

With the use of cubic splines, the data can be represented by a smooth curve as seen in the weekend news reports:

|

|

|

Suppose a set of (n+1) data points is given in the (x,y) plane:

(x1,y1);

(x2,y2); …; (xn,yn); (xn+1,yn+1)

In our case, n = 4. Also the

points are equally spaced in the x-direction, such that the distance between

the x-coordinates (step size) is:

h = x2 -x1

= x3 -x2 = … = xn+1 -xn

Let

y = S(x) denote a smooth interpolating curves that connects the

given data points. The cubic spline interpolant y = S(x) consists

of cubic polynomials y = Sj(x) that connect two

consecutive data points: (xj,yj) and

(xj+1,yj+1):

y = Sj(x) = aj

+ bj (x - xj ) +cj (x – xj)2

+ dj (x – xj)3, xj < x < xj+1

Coefficients

(aj,bj,cj,dj) are

found from the conditions that piecewise cubic spline interpolants y = Sj(x)

form a continuous curve with continuous first and second derivatives at

all points. Both the slopes and the curvatures of the interpolants y = Sj(x)

are matched continuously, so that the resulting interpolating curve y

= S(x) shows up as a smooth curve in viewer's eyes. Eyes of a viewer

cannot distinguish any sudden changes in third and higher derivatives of the

curve y = S(x).

Denote

mj = Sj''(xj) for j =

1,2,…,n,n+1. The coefficients (aj,bj,cj,dj)

of the cubic spline interpolants y = Sj(x) are

found from the values of mj as:

aj = yj

, bj = ![]() -

- ![]() h, cj

=

h, cj

= ![]() , and dj =

, and dj = ![]()

The

values of mj are found from a system of (n-1) equations:

mj-1 + 4 mj

+ mj+1 = ![]() ( yj-1 – 2 yj + yj+1 ), j = 2,…,n

( yj-1 – 2 yj + yj+1 ), j = 2,…,n

The

linear system is under-determined, since two values of mj are

still unknown and two more equations have to be added to the system of (n-1)

equations. There are several ways to specify the two additional conditions

required to obtain a unique cubic spline through the points: (i) natural

spline, (ii) parabolic runout spline, and (iii) cubic runout spline.

Objectives:

·

understand

the algorithm for setting cubic spline interpolants with different end-point

conditions

·

exploit

the cubic spline interpolation and achieve the best visualization of the market

weekly reports

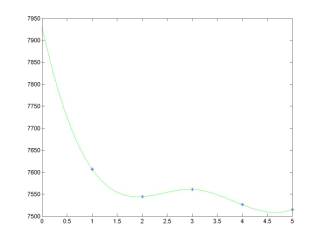

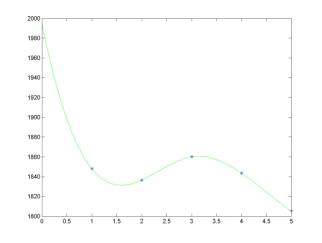

MATLAB script for natural cubic spline interpolation:

The

natural cubic spline interpolation is prescribed by the end-point conditions:

m1 = 0; mn+1 = 0

The

natural spline conditions are equivalent to the conditions that the second

derivative of the cubic spline y = S(x) is zero at the end

points. Thus, the natural spline approaches to the end points x = x1

and x = xn+1 as a straight line. The natural

spline tends to flatten the interpolating curve at the end points, which may be

undesirable:

|

|

|

The

linear system for values of mj (j = 2,…,n) for natural

spline interpolation is set in the matrix form: A m = b, where

A =  , m =

, m = ![]() , b =

, b = ![]()

Steps

in writing the MATLAB script:

- Assign the given data

values to vectors x for weekdays, y for TSE300

index, and z for NASDAQ index.

- Initialize and compute

the coefficient matrix A and the vector of right-hand-sides b

for each data set.

- Compute the values of mj

for j = 1,2,…,n,n+1 for each data set.

- Compute coefficients (aj,bj,cj,dj)

of the cubic spline interpolants y = Sj(x).

- For two data sets, plot

the cubic spline interpolants for a small-sized partition xint

between [0,5], where 0 stands for

Monday opening bell and 5 stands for Friday closing bell.

- Plot points of the corresponding data sets at the same graphs.

Exploiting

the MATLAB script:

Compute the values of the cubic spline interpolant

in middle of Wednesday.

Answer: In the middle of Wednesday: TSE 300 = 7551.66; NASDAQ = 1848.57

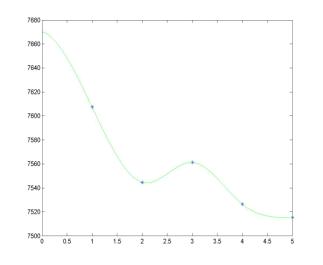

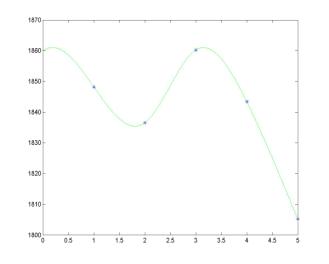

MATLAB script for parabolic runout spline interpolation:

The

parabolic runout spline interpolation is prescribed by the end-point

conditions:

m1 = m2; mn+1 = mn

The

parabolic runout spline conditions are equivalent to the conditions that the

spline y = S(x) reduces to a parabolic curve on the first and

last intervals. Thus, the parabolic runout spline approaches to the end points x

= x1 and x = xn+1 as a parabolic

curve. The parabolic runout spline is neither flat nor curved at the end

points, i.e. it may be a reasonable compromise for a better visualization of

the interpolating curve:

|

|

|

The

linear system for values of mj (j = 2,…,n) for

parabolic runout spline interpolation is set in the matrix form: A

m = b, where

A =  , m =

, m = ![]() , b =

, b = ![]()

Steps

in writing the MATLAB script:

- Assign the given data

values to vectors x for weekdays, y for TSE300

index, and z for NASDAQ index.

- Initialize and compute

the coefficient matrix A and the vector of right-hand-sides b

for each data set.

- Compute the values of mj

for j = 1,2,…,n,n+1 for each data set.

- Compute coefficients (aj,bj,cj,dj)

of the cubic spline interpolants y = Sj(x).

- For two data sets, plot

the cubic spline interpolants for a small-sized partition xint

between [0,5], where 0 stands for

Monday opening bell and 5 stands for Friday closing bell.

- Plot points of the corresponding data sets at the same graphs.

Exploiting

the MATLAB script:

Compute the values of the cubic spline interpolant

in middle of Wednesday.

Answer: In the middle of Wednesday: TSE 300 = 7552.95; NASDAQ = 1849.30

QUIZ: "MATLAB script for cubic runout spline interpolation:

The

cubic runout spline interpolation is prescribed by the end-point conditions:

m1 = 2*m2 -m3; mn+1 = 2*mn -mn-1

The

cubic runout spline conditions are equivalent to the conditions that the spline

y = S(x) reduces to a single cubic curve on the first two and

last two intervals. Thus, the values of m1 and mn+1

are extrapolated from inside conditions that the first two cubic spline

interpolants y = S1(x),y = S2(x) and the

last two cubic spline interpolants y = Sn-1(x),y = Sn(x)

coincide identically. The cubic runout spline produces a curve with pronounced

curvature at the end points, which may be undesirable. The linear system for

values of mj (j = 2,…,n) for cubic runout spline

interpolation is set in the matrix form: A m = b, where

A =  , m =

, m = ![]() , b =

, b = ![]()

Steps

in writing the MATLAB script:

- Assign the given data

values to vectors x for weekdays, y for TSE300

index, and z for NASDAQ index.

- Initialize and compute

the coefficient matrix A and the vector of right-hand-sides b

for each data set.

- Compute the values of mj

for j = 1,2,…,n,n+1 for each data set.

- Compute coefficients (aj,bj,cj,dj)

of the cubic spline interpolants y = Sj(x).

- For two data sets, plot

the cubic spline interpolants for a small-sized partition xint

between [0,5], where 0 stands for

Monday opening bell and 5 stands for Friday closing bell.

- Plot points of the data sets at the same graphs.

Exploiting

the MATLAB script:

- Compute the values of

the cubic spline interpolant in middle of Wednesday.

- Use MATLAB function

"spline" to compute the values of the spline interpolant

in middle of Wednesday.

- Compute the norm of the

difference between the cubic spline interpolants produced by MATLAB

function "spline" and by the cubic runout spline. Show

that the MATLAB function "spline" uses in fact the cubic

runout spline conditions.